This article is for those valuing a share sale for a mid-market private business. It is crucial to understand the offer’s net asset position at settlement before you can understand the total value of a share offer to the seller or buyer.

Mid-market business prices are usually expressed as “Price plus SAV” (stock at valuation). The presumption is that the purchaser’s lawyer strongly advises not to buy shares because there are unknown liabilities attached to the limited liability company that you may be exposed to. Lawyers prefer asset sales to avoid unknown liabilities—the buyer’s own limited liability company buys the assets including intangible assets and assigns any agreements to the new company.

However, there are times when the benefits of buying the shares of the company outweight the costs, only a part of the company is being sold, or you are comparing an asset sale offer from one party to a share sale offer from another.

Share Sale Offers Require “Net Assets” Term

In a share sale case there are two key price elements that must be provided:

- the offer price

- the balance sheet at settlement

Offer Price. The offer price is simply expressed as a dollar amount for a % of shares, e.g. $19 million for 100% of shares.

Balance Sheet at Settlement. Understanding the balance sheet at settlement is really about what dividend the owner can pay at or before the settlement date.

On the one side, a smart purchaser may demand a balance sheet that does not allow for any dividends or special dividends, increasing balance sheet net asset position at settlement.

On the other side the owner wants to pay as high a dividend as the balance sheet can stand, reducing the net asset position at settlement. The purchaser may want no dividend paid so they get more assets for their offer price. There is often a tension between the two or sometimes a lack of knowledge by one party who only thinks of the headline offer price.

A seller could strip the company of assets before settlement resulting in the purchaser needing to add additional capital in to the business on day 1 of ownership. A purchaser could quietly assume significant retained earnings that could have been distributed to the seller along with the share value.

Example

I’ll demonstrate the concept using an example.

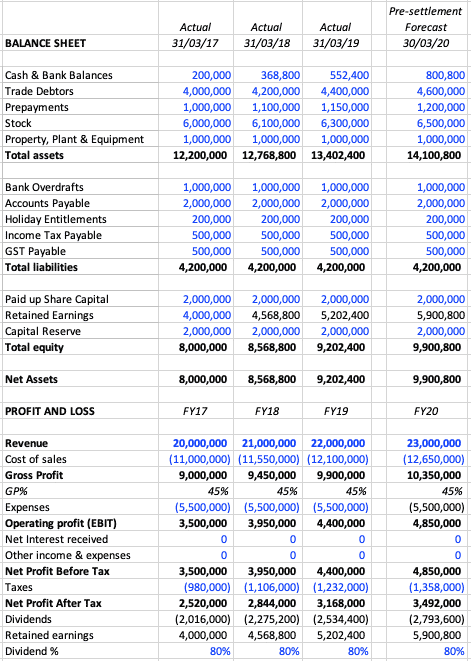

A share offer is made for the business, price of $19M (M=million). Below is the Balance Sheet and Profit & Loss actual last 3 years and forecast for the current year. Blue figures are input data, black figures are calculations.

Figures below:

Balance Sheet and P&L: actual FY17-19 and current year forecast FY20

Forecast balance sheet is day before settlement.

This covers the last 3 years actual plus a forecast for the current FY20 year.

In order to keep things simple:

- I haven’t increased liabilities

- I have increased various asset lines by an amount of the retained earnings of the previous year

- I have ignored interest recevied and payable, other income and expenses

Dividend Policy and Retained Earnings

I have assumed that the divided payout policy is 80% of NPAT. Importantly this increases retained earnings by adding the retained earnings of the previous year plus NPAT less dividends.

The point here is that the business retains some of the profit on the balance sheet rather than distributing it as dividends. The seller could reasonably argue that they build up equity in the balance sheet for them to distribute as a dividend or spend on the company in the future. They are about to sell the company so they want to hand the company over post a final distribution of this retained earnings—but this is not a rule just an opinion or negotiation position.

Add Normal Dividends to the Price

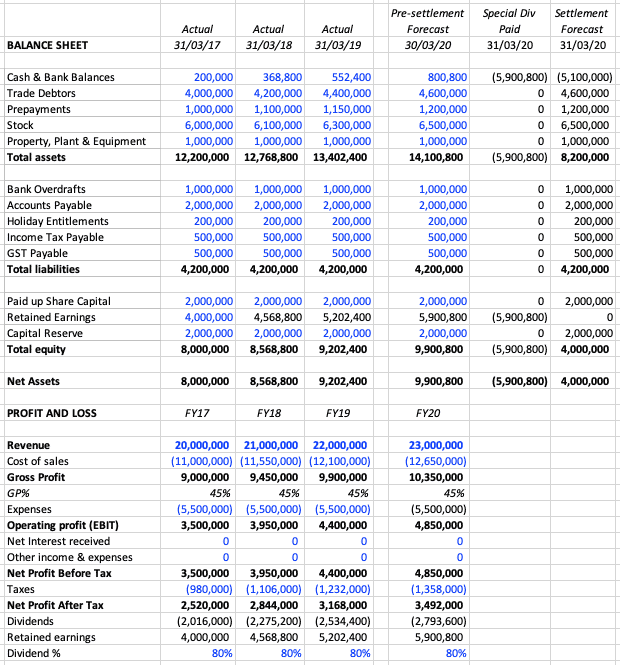

The first thing to point out is that if the company declares a dividend payout for FY20 as per its normal 80% of NPAT then the seller will receive $2,793,600 on top of the Total Price of $19M. So the value they receive is $21,793,600 in this transaction not $19M.

The share offer would be described as $19M with Net Assets at Settlement of $9,900,800.

Add a Special Dividend to the Price

However, the seller also wants to pay a special dividend to clear out retained earnings so a special dividend is declared on settlement day of $5,900,800 on top of the normal dividend above. The total value is now $27,694,400 = $19M plus a normal dividend of $2,793,600 plus special dividend of $5,900,800.

The share offer is now described as $19M with Net Assets at Settlement of $4,000,000.

Exactly which line the dividend is paid from would be based on your accountant’s advice but for our M&A purposes we just leave it as a negative cash balance (it could be a loan in the liabilities instead perhaps).

Figures below:

Balance Sheet and P&L: actual FY17-19 and current year forecast FY20

Forecast balance sheet now includes the settlement date.

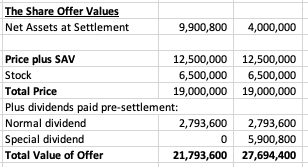

Total Price is just a Headline

The Offer Price has remained the same but the Total Value of the Offer is much different as the table below shows.

Figure: The Share Offer Values

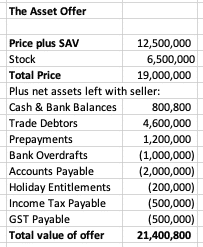

Asset Price

Let’s finish this off by comparing the Asset offer to the Share Offer. The asset price also has additional net assets that should be included.

An asset offer would usually state that the seller keeps the trade debtors. They also keep the rest of the assets and liabilities post settlement.

In this case it would look like the Figure below.

Figure below: Asset Offer Total Value

There is no need to make a decision about dividends as you keep the company shares and just sell the assets including intangible assets.

You can see this means you keep cash, net trade debtors, overdraft and other liabilities. This nets an additional $2.1M.

Summary

What dividends you can declare out of the company is a key part of any share offer. This is described as net assets at settlement date. It the example above it added up to 45% to the total value of the offer. Received a share offer—always ask the second question what are net assets at settlement date?